When applying for a housing loan in Singapore, you need to have an understanding of the Total Debt Servicing Ratio (TDSR). This article will introduce the definition of TDSR, how it is calculated, and how it impacts your housing loan.

What is TDSR?

The Total Debt Servicing Ratio stipulates that only up to 55% of a borrower's total monthly income can be used to repay debts. These debts include housing loans (including the loan being applied for), car loans, credit card debts, and other personal loans.

The Singapore government introduced the TDSR framework in 2013 to ensures that borrowers' debts remain within their affordable range and financial institutions lend responsibily. Meanwhile, it is also aimed at curbing real estate speculation. In the past, many individuals borrowed large sums of money to purchase properties beyond their own capabilities, intending to make a profit by reselling them. Overall, TDSR helps prevent the issuance of high-risk loans and provides banks with a standardized framework to assess borrowers' repayment capacity.

All banks and financial institutions must comply with the existing TDSR regulations when assessing the following loans:

• Housing loans

• Refinancing of housing loans

• Loans secured by property

However, TDSR exemptions applies in the following situations:

• You are looking to refinance an existing property loan (it must be a owner-occupied property)

• You will obtain a small loan secured by multiple properties (as collateral), and the loan amount is less than half of the market value of the properties.

• You will obtain a bridging (short-term) loan that you will repay within 6 months.

• You obtain a loan for a property with a loan-to-value ratio of less than 50% (the loan amount is less than half of the property's value).

How the TDSR Affects Your Housing Loan

TDSR applies to the purchase of all types of residential properties. TDSR limits the amount you can borrow, that is, your loan amount, by stipulating that your monthly debt repayment cannot exceed 55% of your monthly income. The more debts you have, such as student loans, car loans, credit card bills, personal loans, etc., the smaller the housing loan amount you may obtain from the bank.

How to Calculate TDSR

The TDSR formula is as follows:

(Borrower’s total monthly debt obligations / Borrower’s gross monthly income) x 100%

If you’re taking out a loan with someone else as a joint borrower, then the TDSR will be calculated based on the following:

• Aggregate gross monthly income of both borrowers

• The debt obligations of both borrowers

• The loan tenure, which is determined by the income-weighted average age of the borrowers

The calculation of TDSR will also take the following factors into account:

▲Loan tenure rules

The loan tenure is capped at 30 years for HDB properties and 35 years for non-HDB properties.

▲A stress-test interest rate

Currently, it is 4% for residential properties. This means that even if the interest rate rises to 4%, home loan applicants must still be able to maintain a TDSR of 55% or below.

▲Variable Income and Certain Financial Assets

For example, rental income will be calculated at a discounted rate. Freelancers or self-employed individuals are considered higher-risk borrowers due to their unstable incomes; therefore, generally only 70% of this variable income is included in monthly income.

In addition, if you have financial assets such as stocks, unit trusts, bonds, gold, foreign currency deposits, and other liquid assets can be included in your monthly income.

Examples on How to Calculate TDSR

▲Fixed Income

For example, if your monthly income is $10,000,the maximum amount you can use to repay various debts each month is $10,000 × 55% =$5,500. If you also have a car loan of $2,000 and a credit card debt of $1,000 to repay each month, then the amount available for repaying the housing loan will only be $5,500 - $2,000 - $1,000 =$2,500.

▲Variable Income

Suppose your fixed monthly income is $7,000, and you also have a monthly rental income of $3,000. Then only $3,000 × 70% = $2,100 of your rental income will be counted into your monthly income. Therefore, your total monthly income is $7,000 + $2,100 = $9,100. If your total debt at this time is $3,000, then your TDSR = $3,000 / $9,100 = 33%.

▲Joint Applications

Suppose you have a fixed monthly income of $3,000 and monthly debts repayments of $1,000. Your husband's gross monthly income is $5,000, and his total monthly debts repayments are $2,000.

The TDSR of the joint application = (Total monthly debt obligations)/(Gross monthly income) = $3,000 / $8,000 = 37.5%

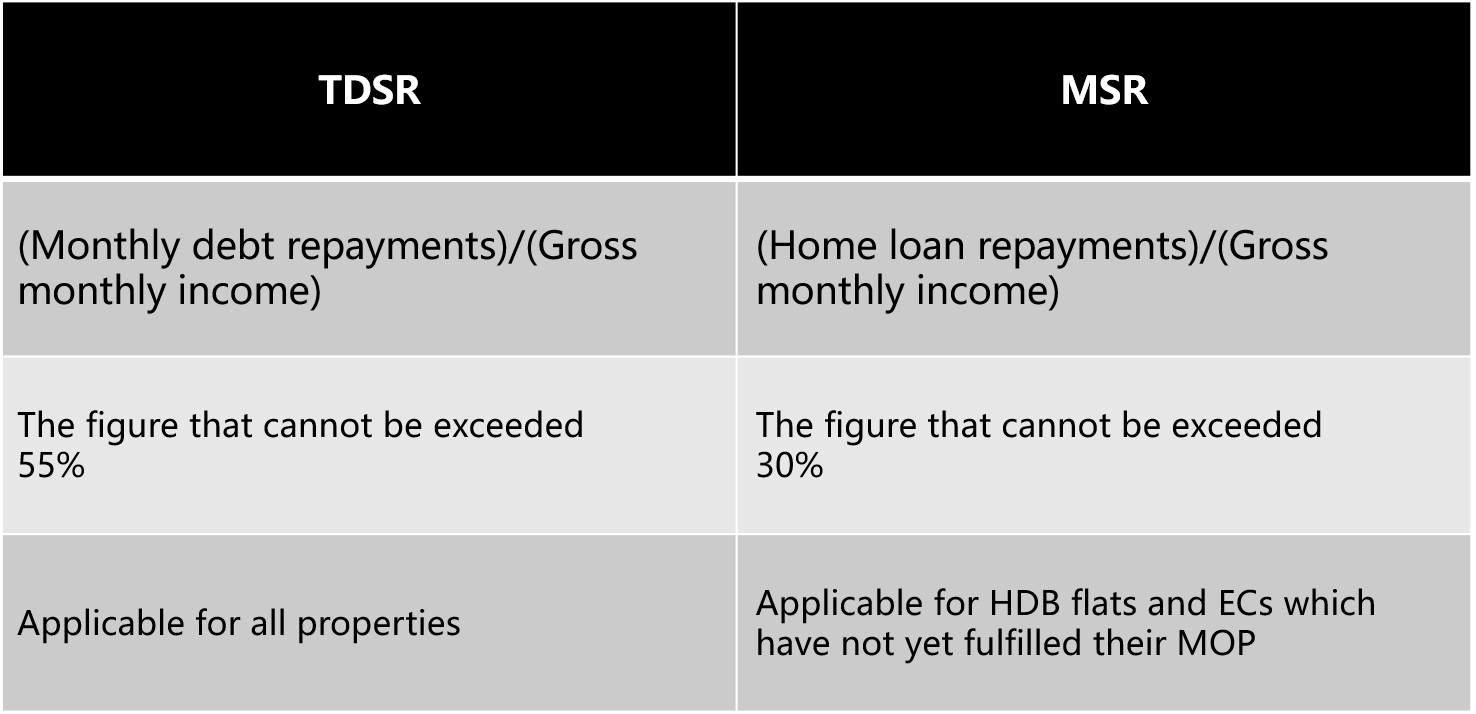

TDSR vs MSR

TDSR applies to the purchase of all types of residential properties. If you are purchasing a HDB flat or an Executive Condominium (EC), in addition to TDSR, you must also consider the Mortgage Servicing Ratio (MSR).

The Mortgage Servicing Ratio (MSR) refers to the proportion of the borrower's total monthly income used to repay the housing loan. Currently, the maximum MSR Limit is 30%. For example, if your monthly income is $10,000, you can only use $3,000 of it to repay the housing loan .

TDSR and MSR considers different financial factors. TDSR considers all the borrower's outstanding debts, including housing, car, education, credit card loans, etc. In contrast, MSR is simpler as it is calculated solely based on the borrower's monthly income. For borrowers purchasing HDB or EC units, MSR will be used for the initial assessment first to calculate the maximum amount they can repay each month. After that, a second round of assessment will be conducted on the buyers to determine whether all their debts to be repaid fall within the TDSR limit. If the borrower has outstanding debts (such as a car loan), it may affect their borrowing amount, and they may not be able to secure the maximum MSR loan amount.

If your TDSR and MSR are too high, you can explore the following options to reduce them:

▲Repay existing debts to improve your borrowing capacity and potentially qualify for a larger loan.

▲Refinance existing loans at a lower interest rate to reduce monthly repayments.

▲Look for ways to generate additional income, such as freelancing or renting out spare rooms.

▲Consider smaller and/or more affordable properties.

For more questions related to bank housing loans, such as loan eligibility, processing procedures, and interest rates, etc., you can check the articles on Housebell:

Singapore House Purchase: A Guide to Bank Loans