When purchasing a property in Singapore, most people will consider taking out a mortgage. The interest rate is a very important factor, as it directly affects the monthly repayment amount and also significantly impacts the overall property purchase cost and financial planning. This article provides an overview of the latest mortgage interest rates in Singapore and related considerations.

The Latest Mortgage Interest Rates in Singapore

In early 2023, the mortgage interest rate in Singapore was as high as 4.25%. Since 2024, the fixed mortgage interest rate has declined, dropping from a maximum of 4.25% to a minimum of 2.45%. As of December 2024, the fixed mortgage interest rates offered by banks in Singapore range from 2.45% to 2.8%, which are at a relatively low level worldwide.

The benchmark for floating rates, the three-month compounded Singapore Overnight Rate Average (SORA), has also been on a downward trend, falling from 3.7012% on January 2nd to 3.1232% on December 23rd.

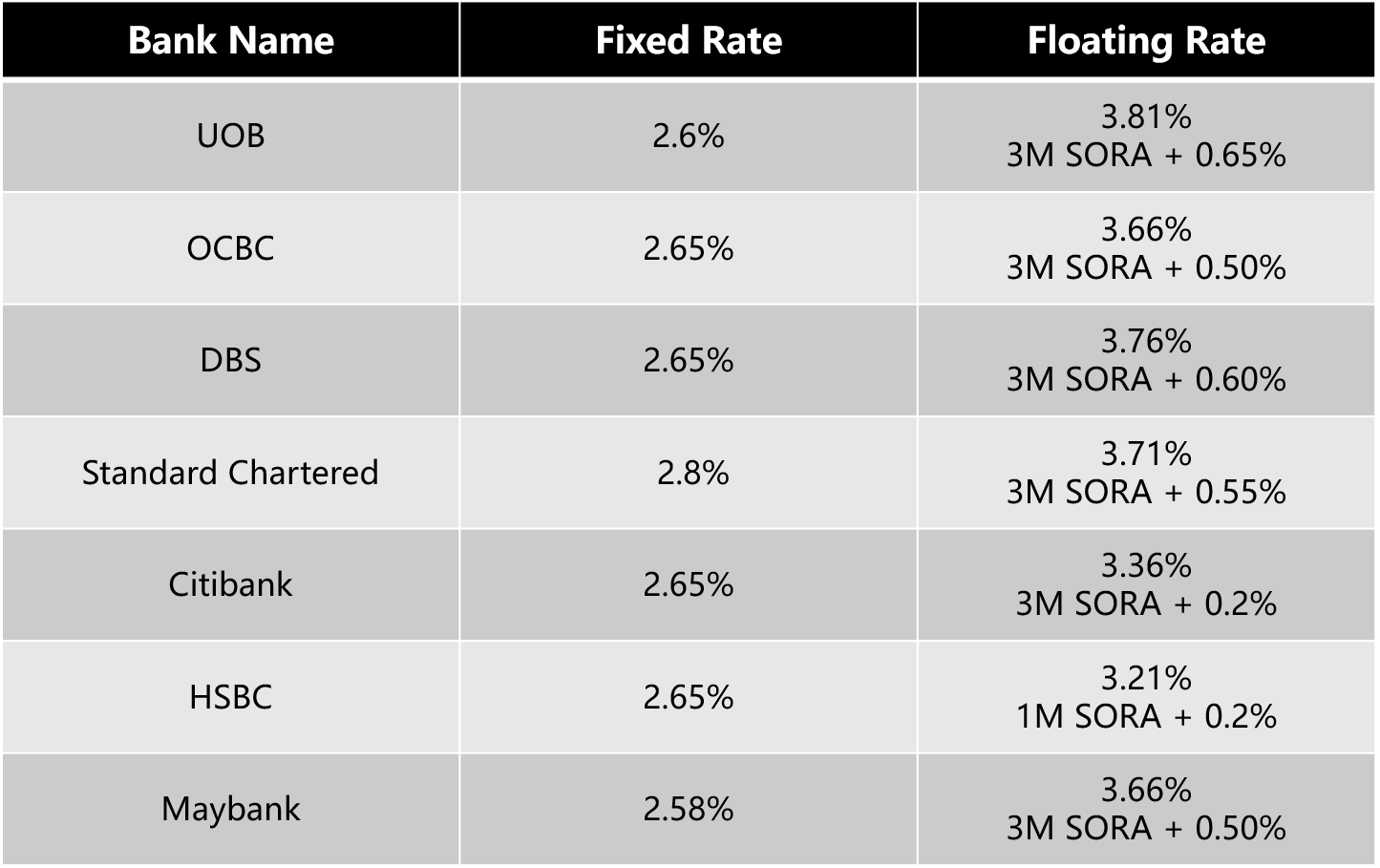

Currently, the average mortgage interest rate in Singapore is between 2.5% - 2.8%. The following table shows the condo mortgage interest rates of some common banks for reference . (Updated on December 24, 2024)

*Note: Rates are subject to change; please consult the respective banks for the most current information.

Fixed Rate and Floating Rate

There are two modes for mortgage interest rates: fixed rate and floating rate.

Fixed Rate

During the entire loan period, the loan interest rate remains unchanged. In case the market interest rate rises later, you can still maintain a lower interest rate and save on interest payments. However, if the market interest rate drops later, you will need to pay more interest than others. The main advantage of the fixed rate is its stability; you don't need to constantly monitor interest rates changes. It is suitable for homebuyers with relatively fixed incomes or those who don't want to worry about rate fluctuations. Generally, the fixed rate will be slightly higher than the floating rate available on the market in the same period. However, during a period where interest rates are expected to rise, choosing a fixed rate may be a better option than a floating rate.

Floating Rate

It fluctuates according to the changes in a sepcific benchmark interest rate (SORA rate). Floating rate = SORA + Spread (adjustment spread). The primary advantage of a floating rate is that it is relatively flexible. If the benchmark interest rate drops, the monthly repayment amount will also decrease accordingly. However, during the period when the interest rate rises, the monthly repayment amount under the floating rate will be significantly higher than under a fixed rate. Therefore, when interest rates are expected to fall, people usually prefer to choose the floating rate.

Note: For new condominiums that are still under construction (Pre-selling properties), banks only offer floating rate schemes and do not provide fixed rate schemes. After the condominium is completed, there is usually an opportunity to change the scheme for free.

How to Choose the Interest Rate Mode and the Lending Bank

Fixed Rate or Floating Rate?

Consider the stability of personal income. If the income is stable and you are sensitive to interest rate fluctuations and hope to avoid the risk of rising interest rates, the fixed rate is a more suitable choice; if your income has a certain degree of flexibility and you can bear the risk of interest rate fluctuations, and expect to benefit when interest rates fall, the floating rate is more attractive.

Secondly, it is also necessary to predict the trend of market interest rates trends. Although it is extremely challenging to accurately predict the direction of interest rates, reasonable judgments can be made to a certain extent by paying attention to factors such as the macroeconomic situation and the orientation of monetary policy.

In addition, homebuyers should also align their own property purchase budgets, loan tenure, and long-term financial plans. Weigh the pros and cons of different interest rate models to make decisions that best suit their circumstances.

Factors to Consider When Choosing Bank Packages

★Interest Rate Level

Compare the interest rate packages of different banks and consider banks with lower interest rates to save on interest.

★Loan Term

If the loan term is long, the fixed rate can lock in costs and avoid the risk of repayment pressure caused by large fluctuations in future interest rates. If the loan term is short, the floating rate can be chosen according based on interest rate trend. Meanwhile, pay attention to the banks interest rate policies and terms for different loan periods.

★Loan Packages and Services

Some banks may offer additional benefits and services, such as free financial consulting, repayment reminders, and flexibility for early repayment when selling the property, etc.

★Eligibilities and Requirements

Different banks may have different requirements for customers' income levels, credit records, occupations, etc. You need to ensure that you meet the bank’s loan condition. Some banks may offer more favorable interest rates or higher loan amounts to people in specific occupations or high-income groups.

★Bank Reputation and Stability

Choose banks with good reputations and stable financial conditions to ensure the smooth progress of the loan process and the quality of follow-up services. You can refer to the bank's ratings, market reputation, and business history in Singapore, etc.

★Refinancing Policy

Understand the refinancing policies of banks, including the maturity date of the package lock-in period, the notice period, whether handling fees and early repayment penalties are charged, as well as the refinancing process and conditions. If there is a possibility of refinancing in the future, choose banks with relatively lenient policies and lower costs.

★Bank Branches and Convenience

Consider whether the bank branches are convenient for daily repayment, consultation, and handling of related transactions. As well as evaluate whether the online banking and mobile banking services of the bank are user-friendly.

For more questions related to bank housing loans, such as loan eligibility, processing procedures, and interest rates, etc., you can check the articles on Housebell:

Singapore House Purchase: A Guide to Bank Loans